A pattern seems to be emerging across the original equipment manufacturers, or OEMs, who have been largely waiting on the sidelines to get into the generative AI riches story. Nvidia is making money, and now AMD is, too. HBM memory suppliers are making money, and so is the Taiwan Semiconductor Manufacturing Co chip foundry.

But, as has often been the case with traditional HPC simulation and modeling workloads over the decades, the companies that make scale-out clusters for massive compute jobs like AI training and now inference could not get very many GPU allocations during the past two years of the GenAI boom, so they didn’t make any money – meaning, they did not generate profits – because they didn’t really have anything in the way of AI server, storage, or networking revenues. And now that the OEMs are finally able to get some GPU allocations, they are beginning to drive sales, but they do not seem to be able to make money on this ridiculously expensive iron. Which is, well, ironic.

As we have previously reported in the most recent financial reports from Hewlett Packard Enterprise and Dell Technologies, the datacenter businesses have been under pressure from a recession in sales of general purpose servers and are now starting to see signs of recovery even as they are finally able to take down some of their AI server backlogs from customers who have been tapping their feet to get going on GenAI. It is hard to say for sure whether the AI businesses of either HPE or Dell are is unprofitable, running at breakeven or moderately profitable because these companies – as well as their compatriot in the OEM racket, Lenovo – do not break their AI server operating income out separately from their overall datacenter businesses.

It is important to not jump to the conclusion that the AI server businesses of Dell, HPE, and Lenovo are unprofitable. And many have done this in the past two weeks as these three companies reported their financial results.

That said, there certainly precedence from the adjacent HPC simulation and modeling hardware business that the OEMs never really make money and the component suppliers that feed them do. SGI, Cray, and IBM all had fairly large HPC businesses, but averaged over the long haul, they might have only been moderately profitable to the tune of a point or two of revenues.

This is kind of margin that warehouse retailers get, or the big original design manufacturers get. (ODMs take server designs from the hyperscalers and cloud builders and make machinery to spec at high volume and very low margin.) In theory, and in practice for many decades until the rise of the hyperscalers and the clouds, the OEMs could extract some profits from small and medium businesses who buy machinery in lower volumes (and hence at higher unit prices) and more than cover their costs for relatively deep discounting given to their large enterprise and relatively high volume customers.

Historically, the OEMs made some money on hardware, but they made more money – again, meaning profits – on technical support and sometimes software. IBM, for instance, has an enormous and wildly profitable mainframe software business and a fairly large Unix and proprietary server software business as well as services and financing businesses that hang off of all of this.

This is the model that HPE and Dell and now Lenovo are all emulating, although the HPE and Dell have sold off big chunks of their services businesses over the past decade. IBM followed suit with its Kyndryl outsourcing business two years ago, spinning it off. Lenovo is still building its software and services business, which turns out to be a saving grace during the server recession and during the long wait to start doing GenAI system deals in any appreciable volume.

(Note for history buffs: A very large portion of the Lenovo server business was spun out of IBM a decade ago, and so was a very large portion of Lenovo’s PC business was spun out of IBM two decades ago.)

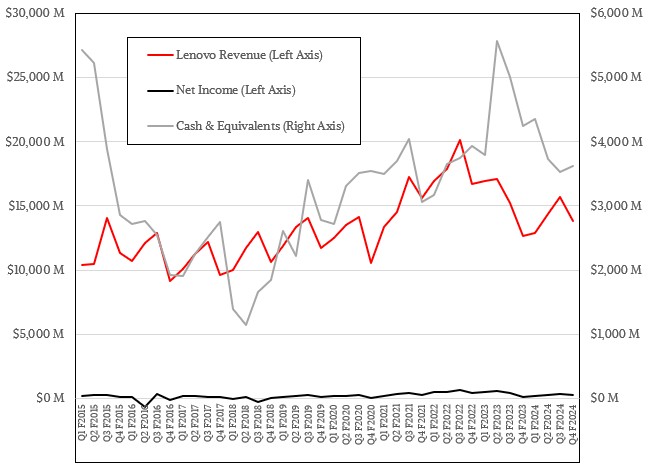

In the quarter ended in March, which is the end of Lenovo’s fiscal year, Lenovo had $13.83 billion in sales, up 9.5 percent year on year, and net income was $248 million, a factor of 2.2X higher than in the year ago period. Lenovo ended the quarter with $3.63 billion in cash and equivalents, which is down 14.7 percent over the fiscal year.

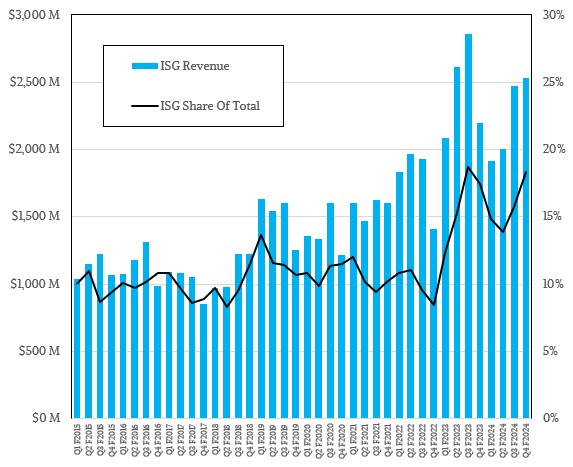

Lenovo’s Infrastructure Solutions Group, which makes datacenter hardware, posted sales of $2.53 billion, up 15.1 percent and, importantly, up 2.42 percent sequentially from Q3 of fiscal 2024.

“The industry-wide challenges, including a shift in demand towards AI causing a short-term, supply-side disruption, weighed on Infrastructure Solutions Group’s performance, leading to a segment loss for the full year,” the company said in a statement accompanying the financial results. “Nevertheless, its efforts in customer acquisition and portfolio expansion facilitated a turnaround, with sales rebounding to positive double-digit growth in the final fiscal quarter, setting the stage for future profitability improvement.”

For the full year, ISG had sales of $8.92 billion, down 8.5 percent compared to fiscal 2023. In fiscal 2023, the general purpose server recession was caused in part by server overconsumption in 2022 and also by a rapid shift to AI spending at IT organizations around the world, and that put pressure on Lenovo’s system profits. In fiscal 2023, Lenovo managed to eke out $97 million in operating income, which was just a smidgen under 1 percent of revenues, while in fiscal 2024 it lost money every quarter and it lost $247 million.

The good news is that Lenovo’s Solutions & Service Group, which peddles software and various kinds of technical and implementation services, had $7.47 billion in sales in fiscal 2024, up 12.1 percent, and posted an operating profit of $1.55 billion, up 11 percent. An increasing amount of that portfolio of software and services is driven by HPC and now AI stuff as well as cloud-priced TruScale as a Service systems that stay on the Lenovo books but are consumed like a public cloud by customers (akin to HPE GreenLake and Dell APEX offerings.) We do not know how much revenue the cloudy TruScale systems are driving, but it would be nice to know.

We would also love to see HPC/AI systems split out formally from regular enterprise-class servers running databases and other kinds of application software, and we would also love to see storage and networking split out from servers. But companies are not interested in giving out too much data about their businesses – just enough to mollify investors is the rule of thumb among the publicly traded.

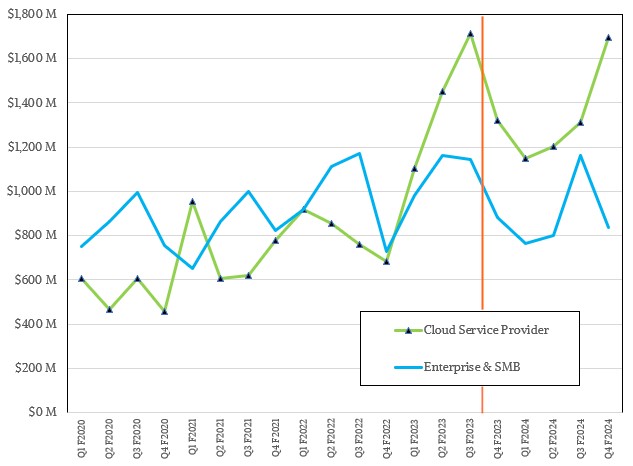

Up until Q3 2023, Lenovo used to break its sales of datacenter iron into two pieces: Cloud service providers – what we here call hyperscalers or cloud builders, depending on the nature of the applications running on the iron – and Enterprise & SMB, which means everybody else. We went back into the archive and plotted out the data from the Lenovo charts, estimating the actual revenues of these by counting pixels in the charts. After seeing this was too much information, Lenovo stopped providing the ISG charts that detailed this, and since that time we have estimated CSP versus ESMB revenues within ISG based on comments the company’s top brass makes. Take these numbers with a grain of salt:

The right of the red vertical line in the chart above has a lot of witchcraft in it, and the left of the red line is more or less data that is good to within a few points of whatever official numbers Lenovo might supply. (You are only as good as the relatively size of a pixel.)

Our best guess is that Lenovo had just a tad under $1.7 billion in server sales to cloud service providers in Q4 F2024m an increase of 28.6 percent year on year and an increase of 29.5 percent sequentially. We think Lenovo’s businesses to non-CSPs was down 5 percent to $836 million in the quarter.

Kirk Skaugen, who used to run Intel’s Data Center Group way back in the day and who has been president of ISG since November 2016, gave a little color on the ISG business on a call with Wall Street analysts, which we used, along with other comments from this call and prior ones, to build our model. Skaugen had this to say:

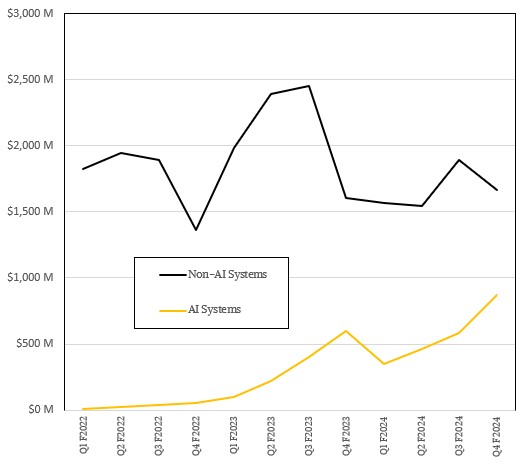

“There’s been a lot of questions about momentum, and then we’ll talk about the architecture. So just a few things that I don’t think we’ve mentioned publicly yet. Our AI server mix for the second half has crossed 29 percent. In the fourth quarter, our AI server revenue was up 46 percent, year-to-year. On-prem and not just cloud is accelerating because we’re starting to see not just large language model training, but retraining and inferencing. So we saw triple-digit growth in our Enterprise and SMB GPU-based server consumption year-on-year.

And our visible qualified pipeline, just since the last quarter, has grown 55 percent and now is over $7 billion. And to kind of put it in perspective, we were public, I think a few earnings calls ago, that we are the exclusive supplier for Nvidia and Microsoft Azure on OVX for Omniverse. But in total, our L40 and L40S Nvidia business just since the first half to the second half of the year is up 270 percent.

So these are incredible growth numbers. Now looking forward, and if you go out to the back, we’ll be time to market with the next-generation Nvidia H200, with Grace Blackwell, with the NVL72. So this is going to put a $250,000 server today with eight GPUs, will now sell in a rack like you’re seeing up to probably $3 million in a rack.”

We had guessed somewhere around $3.3 million for the DGX NV72, so we were in the right ballpark. Skaugen went on to say that Lenovo is “time to market” with AMD MI300X GPU accelerators as well as Intel Gaudi 3 AI accelerators, and was “already in high volume production right now” with the MI300s. Skaugen added that with the Intel “Eagle Stream” and AMD “Genoa” server platforms, which use DDR5 main memory, the company has brought all of its designs in house and that will help with profitability going forward.

That $7 billion AI system pipeline, of course, is what has caught everyone’s attention on Wall Street. What we want to know is what the breakdown of AI versus non-AI servers look like. We took a stab at guesstimating it for Lenovo, and please be aware this is just an informed guess:

With new CPUs coming from both Intel and AMD, with pretty tepid spending last year, and with aging server fleets with machines that are four, five, or six years in the field, everyone is expecting general purpose servers to take off, and we know Lenovo can make money on this if the volumes are high enough.

The question is this: Can Lenovo make money selling GPU accelerated systems to enterprise and midrange businesses that want to control their own AI future? We think there is a chance for this, but only if Nvidia and AMD share some of the margin and don’t keep it all for themselves and expect the OEMs to make their profits on software and services.

No matter what, fear of missing out is the order of the day, and that is true for Lenovo and all of the OEMs as much as it is for every company on Earth. So expect the AI revenue boom to continue, even if profits for the OEMs remain dubious.

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now