The demand for artificial intelligence (AI) software is expected to take off remarkably in the long run as organizations and governments across the globe are deploying this technology for various applications. Not surprisingly, S&P Global Market Intelligence expects the size of the generative AI software market to grow at an annual rate of 58% through 2028, generating $52 billion in annual revenue.

Palantir Technologies (NYSE: PLTR) and C3.ai (NYSE: AI) are two companies through which investors can capitalize on the fast-growing AI software market. However, it is worth noting that both stocks have enjoyed divergent fortunes on the market in the past year. While shares of Palantir have posted impressive gains of 54%, C3.ai stock has dropped 15% in the past year.

Does this mean Palantir is the better AI bet of the two? Or will C3.ai’s fortunes start turning around following its latest quarterly report? Let’s find out.

The case for Palantir Technologies

Known primarily for providing software platforms to intelligence communities and federal agencies for counterterrorism operations, Palantir has now started making good progress in the commercial AI software market. In the first quarter of 2024, Palantir’s overall revenue increased 21% year over year to $634 million. The company’s government revenue was up 16% on a year-over-year basis to $335 million, while commercial revenue jumped at a faster pace of 27% to $299 million.

The growing adoption of Palantir’s AI software platform by commercial customers was a key reason why its commercial revenue grew at a faster pace. Palantir has chalked out a solid go-to-market strategy by conducting “bootcamps,” where it helps customers understand how to deploy AI specific to their use case. On its May earnings conference call, Palantir management pointed out that the company has conducted bootcamps with 915 organizations, and that this outreach is helping it land more customers.

According to Palantir:

As one example, a leading utility company signed a seven-figure deal just five days after completing the bootcamp. Another customer immediately signed a paid engagement after just one day of their multi-day bootcamp and then converted to a seven-figure deal three weeks later. We expect the favorable unit economics and higher throughput to continue to accelerate our business.

This explains why Palantir is witnessing a remarkable surge in bookings from commercial customers. Last quarter, Palantir booked commercial contracts with a total contract value (TCV) of $505 million. That was a massive increase of 187% from the prior-year period. This impressive increase in Palantir’s commercial business is the reason why its remaining deal value (RDV), which is the total remaining value of contracts as of the end of the reporting period, shot up 22% year over year to $4.1 billion.

That was slightly higher than the increase in Palantir’s quarterly revenue. Moreover, the size of Palantir’s RDV suggests that it is building a solid revenue pipeline that should allow the company to maintain a healthy pace of growth in the long run. This is probably one reason why analysts are forecasting the company’s earnings to clock a compound annual growth rate (CAGR) of 85% over the next five years, indicating that Palantir could remain a top AI stock for a long time to come.

The case for C3.ai

C3.ai is another AI software play that’s witnessing an acceleration in growth of late, thanks mainly to a change in its business model where clients pay for its services on a consumption basis instead of entering into long-term subscription contracts. In the fourth quarter of fiscal 2024 (which ended on April 30), C3.ai’s revenue jumped 20% year over year to $86.6 million. Its annual revenue increased 16% to $311 million.

What’s worth noting here is that C3.ai’s revenue growth has been accelerating for the past five consecutive quarters thanks to the growing interest in its AI software offerings. Management points out that its enterprise AI programs are being deployed in 19 industries, and more importantly, C3.ai’s government-related business more than doubled in the previous fiscal year.

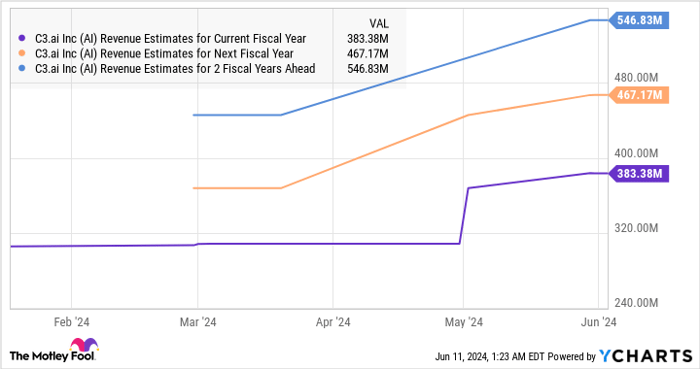

This improving momentum explains why the company’s revenue growth is set to accelerate in the current fiscal year. Also, analysts increased their forecasts for the next couple of years as the following chart indicates.

AI Revenue Estimates for Current Fiscal Year Chart

AI Revenue Estimates for Current Fiscal Year data by YCharts

C3.ai’s improving growth is powered by an increase in the number of agreements the company is closing because of its pay-as-you-go model. In fiscal 2024, it closed 191 customer agreements, a 52% increase over the previous year. Additionally, C3.ai finished the year with 123 pilot projects, which was an increase of 151% from fiscal 2023. This robust improvement in pilot projects could help C3.ai improve its future revenue pipeline if it manages to close those deals.

Thanks to these catalysts, analysts expect C3.ai to maintain a healthy earnings growth rate of 50% for the next five years, indicating that it has the potential to be an AI winner in the long run. The good part is that Wall Street has started realizing C3.ai’s AI potential and the stock surged impressively following its latest report.

The verdict

Both companies are making good progress in the AI software market. However, C3.ai is way cheaper with a price-to-sales ratio of 11.5 as compared to Palantir’s sales multiple of 23. Given that both companies are logging almost identical growth, investors looking for a value play among these two AI stocks are likely to choose C3.ai.

But at the same time, investors with a larger risk appetite may consider buying Palantir as well considering that it is the bigger company of the two and has already built a solid revenue pipeline that could accelerate its growth in the future. Also, as the discussion above indicates, Palantir’s bottom line is expected to grow at a much faster pace over the next five years.

So, investors looking to add an AI software stock to their portfolios have two solid options in front of them, and they can take their pick depending on their risk profiles and the valuation they are comfortable with.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $794,196!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of June 10, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool recommends C3.ai. The Motley Fool has a disclosure policy.

Market Size to Achieve USD 3,680.47 Bn by 2034")