Like many other suppliers of hardware and systems software, Cisco Systems is trying to figure out how to make money on the AI revolution. Thus far, like its OEM and ODM peers, Cisco has had some success building up an AI pipeline, but it is measured in single digit billions of dollars – nothing like the $90 billion or more that Nvidia will likely generate from its datacenter business this year.

That dichotomy tells you that the hyperscalers and cloud builders, plus a few key players like Tesla, represent the bulk of the AI investment even two years after the GenAI explosion. And it remains to be seen when enterprises, governments, and research institutions – particularly the Top 50,000 that have always been the focus of The Next Platform – will get out the checkbooks and start spending on AI initiatives in a way that moves the revenue and profit needles significantly for companies like Cisco.

But, according to the top brass at Cisco, this is starting to happen.

“We continue to capitalize on the multi-billion dollar AI infrastructure opportunity,” Chuck Robbins, chief executive officer at Cisco, said on a call with Wall Street analysts going over the numbers for the fourth quarter of fiscal 2024 ended in July. “We have now crossed $1 billion in AI orders with webscale customers to date, with three of the top four hyperscalers deploying our Ethernet AI fabric, leveraging Cisco validated designs for AI infrastructure. We expect an additional $1 billion of AI product orders in fiscal year 2025.”

“As I shared at our Investor Day in June, this momentum is being fueled by multiple use cases in production with the hyperscalers, several of which are in AI. In addition, we have multiple design wins, with roughly two thirds of these in AI. Over and above the webscale AI opportunity, we believe we are well-positioned to be the key beneficiary of AI application proliferation in the enterprise.”

Most of the AI-related sales, according to Cisco, have to do with back-end Ethernet fabrics and optics used for AI training networks. This means sales of Silicon One ASICs that support AI workflows as well as whitebox switches and even Cisco-design boxes and related transceivers.

These hyperscale and cloud builder customers design their own systems and have them manufactured under contract. Enterprises do not have the scale to be able to afford to do this, and this is one of the reasons why Cisco has been able to build up a base of over 90,000 customers in the past fifteen years for its Unified Computing System blade and rack servers, which fuse compute and networking into a single, virtualized platform. With UCS, customers get many of the benefits of hyperscale servers, but leave the engineering work to Cisco.

It has been a long time since Cisco has talked specifically about the financials of its UCS business, but there are indications that enterprises are spending money on servers and switching in anticipation of adding AI functionality to their applications. These deals are not part of the $1 billion in sales that Robbins talked about above, and are similarly not part of the $1 billion expected for fiscal 2025. More specifically, Robbins says that some enterprises are taking money they had allocated to AI projects and reallocating them back to core infrastructure upgrades – both networks and servers – so they can be ready for AI when they figure out what they are going to do. This was the first quarter that Cisco saw this behavior.

This was also the last quarter that Cisco will be burning down a part of its massive backlog of equipment orders that built up thanks to the supply chain tangles caused by the coronavirus pandemic. Starting in the current quarter, the compares are going to get hard.

In Q1 F2024, Cisco converted somewhere between $3.5 billion and $4 billion of that backlog to revenues, and it will not have that bump this time around in Q1 F2025. Even with the Splunk data analytics and security platform helping to boost revenues – the $28 billion deal closed at the end of March and has contributed $1.4 billion in sales over those four months – it is not enough to fill in that gap.

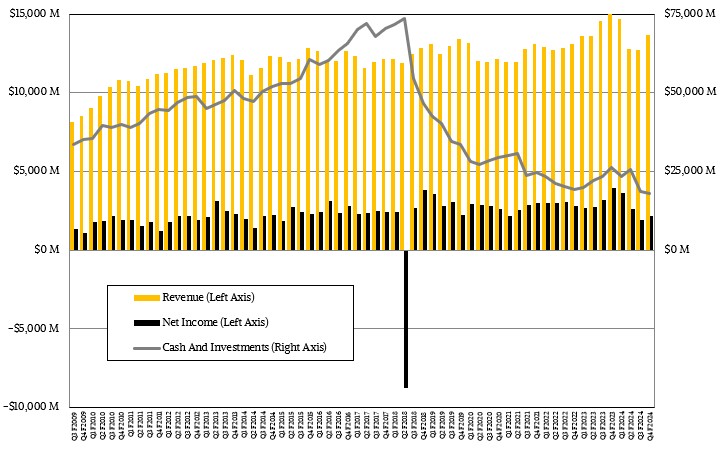

In the July quarter, Cisco’s revenues dropped by 10.3 percent to $13.64 billion. Operating income declined an even faster 38.4 percent to $2.62 billion and net income fell faster by 45.4 percent to $2.16 billion. That net income as a share of revenue was 15.8 percent, which is seven to ten points lower than Cisco’s average.

And so when the company says that it is not cutting 7 percent of its workforce because it needs to cut costs, we don’t believe it. Cisco is investing heavily in AI and is taking down hyperscale and cloud builder business that is no doubt weakening its margins. When pressed, Cisco said that what it is really doing is rebalancing its workforce, moving some jobs to lower cost locations and also investing more heavily in areas of security, cloud, and AI. With margins under pressure and revenue looking to be harder to come by due to a diminished backlog in fiscal 2025, we think Cisco is trying to cut costs and boost profits while also making investments. The good news is that enterprises are starting to spend again on infrastructure, and that will help.

Cisco’s Networking group, which includes switching, routing, and serving, accounted for $6.8 billion, but fell by 28.1 against that bubble last year. Datacenter witching had double digit order growth, and enterprise routing, campus switching, and wireless orders “were also strong,” according to Robbins. The HyperFabric AI cluster based on Nvidia GPUs, which we profiled back in June, have not even started their trials as yet with customers, much less contributed to revenues in this group.

Rounding out the rest of the Cisco businesses, the Security group had $1.79 billion in revenues, up 81.1 percent; the Collaboration group had $1.02 billion in sales, down four-tenths of a point; the Observability group had $249 million in sales, up 40.9 percent; and the Services group had $3.78 billion in sales, up 6.5 percent.

Over the decade and a half that Cisco has been in the systems racket, we have attempted to get a sense of its core datacenter systems business despite all of the organizational and reporting changed, and we continue to do this so we can get a consistent view of that core datacenter business:

As best as we can figure, that core datacenter business of servers, switches, and routing in the datacenter (including service providers, enterprises, hyperscalers, and clouds) posted $6,12 billion in revenues in Q4 F2024, down 28.1 percent, and had an operating income of $1.29 billion, down 50.7 percent. That operating margin of 21.1 percent is lower than the 30 percent or so it has averaged in the past five years.

Featuring highlights, analysis, and stories from the week directly from us to your inbox with nothing in between.

Subscribe now

")