The stock has surged impressively following its recent earnings report.

Shares of C3.ai (AI -0.40%) have underperformed the broader stock market in 2024 with just 4% gains so far, but the artificial intelligence (AI) software provider has gained solid momentum since releasing results in late May for its fiscal 2024’s fourth quarter (ended April 30). The stock has gained 25% since May 29.

Does this mean it is too late for investors to buy shares of a company that looks well-placed to win from the proliferation of AI? Or is now still a good time to buy this AI stock in anticipation of more upside? Let’s find out.

C3.ai’s growth prospects are solid

C3.ai’s revenue in the recently concluded fiscal year increased 16% from the previous year to almost $311 million. The company’s revenue guidance of $370 million to $395 million for fiscal 2025 points toward stronger growth, as the midpoint of that range would translate into a year-over-year jump of 23%.

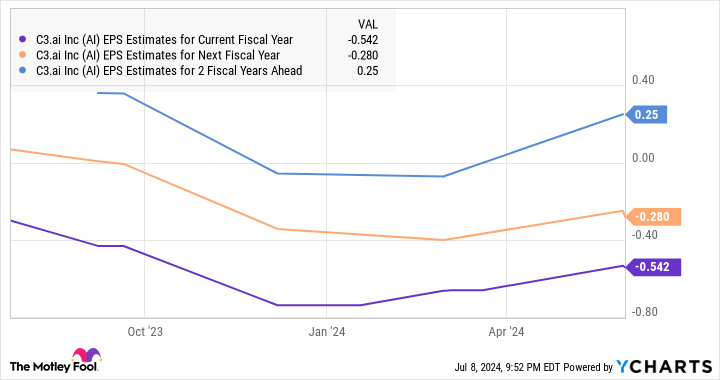

More importantly, analysts have increased their growth expectations from C3.ai for the next couple of years and are expecting the company to clock healthy double-digit growth.

AI Revenue Estimates for Current Fiscal Year data by YCharts.

Even better, the healthy growth in C3.ai’s top line is forecast to translate into impressive growth in its bottom line as well. More specifically, the company’s losses are expected to shrink considerably in the next couple of fiscal years, and it could become profitable in fiscal 2027.

AI EPS Estimates for Current Fiscal Year data by YCharts. EPS = earnings per share.

The key reason C3.ai is expecting an improvement in growth is the strong traction the company’s enterprise AI software is gaining among clients. For instance, C3.ai struck 191 agreements for its enterprise AI software in the previous fiscal year, a big jump of 52% from the previous year.z

It is worth noting that C3.ai’s AI software applications are gaining traction in both commercial and government niches. Half of the company’s bookings in the fourth quarter of fiscal 2024 came from the federal, aerospace, and defense sectors. C3.ai CEO Tom Siebel remarked on the May earnings conference call that the company “had a strong quarter and closed out a remarkable year for the federal business, with revenue growing more than 100% in 2024.”

It won’t be surprising to see C3.ai’s federal AI business grow in the future, as governments across the globe are set to pour billions of dollars into bolstering their AI capabilities. For instance, according to market research firm Canalys, the U.S. government is reportedly considering spending $35 billion on AI-related civilian projects.

Meanwhile, the overall AI software market is forecast to generate annual revenue of $135 billion in 2025, according to Gartner. So, C3.ai is scratching the surface of a massive growth opportunity that could help the company sustain impressive levels of growth in the long run.

The good part is that the company is already engaged in multiple pilot projects with potential clients, which could further improve its revenue pipeline. At the end of the previous quarter, C3.ai was engaged in a total of 34 pilot projects.

Additionally, the company has employed a smart go-to-market strategy by offering its generative AI software applications on the cloud infrastructure platform of popular cloud computing providers, such as Google, Amazon, and Microsoft. This strategy is bearing fruit as C3.ai closed 115 agreements through its cloud partner network program.

In all, C3.ai’s future seems bright, and an improvement in its growth is likely to translate into more upside on the stock market. However, investors would do well to take a closer look at its valuation as C3.ai isn’t exactly cheap following its recent surge.

Should investors buy C3.ai at its current valuation?

C3.ai is now trading at 11 times sales, which represents a premium to the U.S. technology sector’s average of 8.2. The richer multiple the company commands can be attributed to its AI-related growth potential. There is a good chance that C3.ai may be able to justify the same by growing at a faster pace and becoming profitable in the future.

Investors should also note that C3.ai stock doesn’t look expensive when we compare it to fellow AI software play Palantir Technologies, which is trading at 26 times sales and expected to clock revenue growth of 21% in 2024, which will be slightly lower than C3.ai’s estimated growth. All this indicates that investors who haven’t bought C3.ai stock yet can still consider doing so, as it seems capable of delivering more upside, thanks to the growth drivers discussed above.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Microsoft, and Palantir Technologies. The Motley Fool recommends C3.ai and Gartner and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.